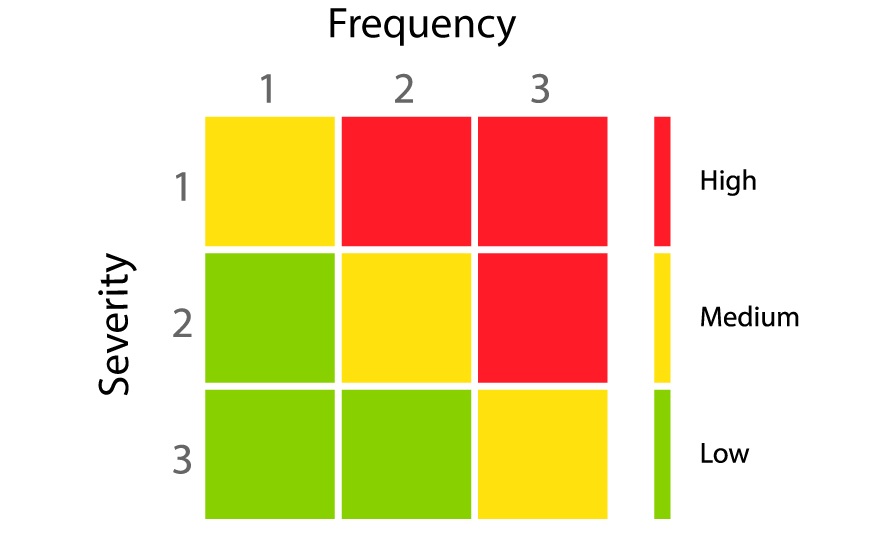

Nearly 60 years ago, a man who was employed by a major American corporation to purchase its insurance published an article that would become a cornerstone of modern risk management. His name was Richard Prouty, and his proposal for how to analyze and evaluate risk exposures has since become canonized as the “Prouty Approach,” which is still taught today in most entry-level risk management training programs. It is frequently expressed pictorially in a graph similar to the one below:

The argument Prouty made was that where the probability and impact of loss can be estimated with some degree of accuracy, prudent risk managers will target those exposures in the middle of the matrix (depicted in yellow) for risk transfer via the insurance mechanism. Those on the low end of the risk spectrum (shown in green) are best retained, while those on the high end (shown in red) are best avoided entirely. Fundamental to this argument is the assumption that extreme risks can be avoided by choice. But what if this assumption is wrong?

The answer to this question is far more than a mere technicality. It is pertinent to every risk manager, insurance advisor, producer, or underwriter in the business of risk transfer. Because if risks are increasing in both frequency and severity AND if they are unavoidable, the implication is that they may only be retained or transferred. Such a conclusion is both frightening and galvanizing; because where underlying conditions are shifting, new challenges and opportunities will be created that produce both losers and winners. Below we offer a few suggestions for maximizing on the growth opportunities for environmental risk management in turbulent times.

First, a statement of simple fact: natural disasters are relied upon for meeting the revenue projections of firms specializing in cleaning up the subsequent messes. While no one would wish a catastrophic wildfire, flood, or windstorm upon any community, when such events do occur, they draw numerous contractors eager to offer their services to restore the affected area. Although this uptick in disaster-related business may not seem like a golden opportunity for environmental insurance, there are multiple pollution exposures tied to smoke, soot, fumes, and mold, as well as the inherent chance for liability associated with the release of asbestos, lead-based paint, or other hazardous materials during structural demolition and debris removal. Restoration contractors are widely eligible for broad coverage packages that include General Liability, Contractors Pollution Liability, and Professional Liability.

Additionally, natural disasters create a perfect opportunity to discuss site-specific pollution exposures that might never have occurred to many property owners or lessees who are convinced they have “no exposure.” What they tend to overlook, however, is that cleanup costs or claims of bodily injury and property damage can be incurred due to pollutants that originate offsite but are deposited on their property by floodwaters, windstorms, or drifting smoke. What’s more, because such events are almost always sudden and accidental, obtaining even limited Site Pollution Liability coverage could provide adequate peace of mind to a wide range of clientele at a very competitive price. For those clients whose onsite operations are riskier, it is worthwhile to review with them their potential for third-party liabilities that could arise if an extreme weather-related event triggered a release impacting nearby properties, persons, or natural resources.

Finally, because a world in which a changing climate is forcing people everywhere to reassess long-held underlying assumptions, it is vital for each person to re-evaluate their own, especially with regard to what constitutes adequate insurance limits. This is no less true for pollution liability insurance than it is for other types of liability coverage. With both Excess and Umbrella policies readily available in the environmental insurance marketplace, and with premiums as competitive and coverages as broad as they have ever been, it is prudent to at least offer higher limit options to your valued clients. Because it just might be possible that Prouty was wrong.

For more information on PartnerOne Environmental and environmental insurance, please contact us.